About JFBAJournal of Fintech and Business Analysis (JFBA) is an open-access, peer-reviewed irregular journal hosted by Beijing Computer Federation and published by EWA Publishing. JFBA serves as a cutting-edge standardized academic platform tracking digital economy evolution, covering normative research on digital growth theory, digital industry evaluation, industrial digital transformation and digital governance, highlighting cross-disciplinary integration, global economic exchange and digital industrial empowerment value alongside core practical application and economic value, and shares frontier analysis models and industrial practice cases for fintech analysts, digital transformation consultants and economics university researchers to translate digital economic research value into industrial practice results. For more details of the JFBA scope, please refer to the Aim & Scope page. For more information about the journal, please refer to the FAQ page or contact info@ewapublishing.org. |

| Aims & scope of JFBA are: ·Digital Economy ·Financial Technology ·Business Analytics |

Article processing charge

A one-time Article Processing Charge (APC) of 450 USD (US Dollars) applies to papers accepted after peer review. excluding taxes.

Open access policy

This is an open access journal which means that all content is freely available without charge to the user or his/her institution. (CC BY 4.0 license).

Your rights

These licenses afford authors copyright while enabling the public to reuse and adapt the content.

Peer-review process

Our blind and multi-reviewer process ensures that all articles are rigorously evaluated based on their intellectual merit and contribution to the field.

Editors View full editorial board

London, UK

canh.dang@kcl.ac.uk

Beijing, China

qingshuiruyuew@gmail.com

London, UK

an.nguyen@kcl.ac.uk

Birmingham, UK

Chinny.Nzekwe-Excel@bcu.ac.uk

Latest articles View all articles

Based on an analysis of the research background, objectives, and significance, this paper employs a variety of research methods to examine the manifestations of credit risk prevention and control in China's banking industry. It further identifies the underlying causes of these risks from four perspectives: the external economic environment, internal banking operations, borrowers, and institutional factors. In response to the emerging trends and challenges facing bank lending, the paper proposes a series of countermeasures, including strengthening risk awareness, enhancing risk management, improving early warning systems, making effective use of credit risk mitigation instruments, implementing sound credit authorization policies, optimizing corporate governance structures, making appropriate dynamic adjustments to credit limits, and reinforcing governance functions, with the aim of improving credit risk prevention and control across China's banking sector.

From ancient bronze coinage to modern blockchain-based tokens, the form of money has undergone a clearly identifiable process of evolution. Yet its fundamental dilemma has remained unchanged: how can a symbol devoid of intrinsic value—the "name"—be made to assume the function of measuring real social wealth—the "substance"? At first glance, the "treasure currency system" introduced by Wang Mang in the late Western Han dynasty appears entirely unrelated to contemporary stablecoins. In essence, however, both confront the same predicament—the separation of name and substance. This study therefore presents a perceptive and logically rigorous comparison of their respective credit mechanisms. Wang Mang's monetary reform ultimately collapsed under the issuance of "nominal values" driven by state power, whereas the central challenge for stablecoins lies in how to anchor their nominal value to credible "substance" within a decentralized framework. From this perspective, the paper naturally arrives at the conclusion that only when name and substance are unified through a credible credit anchor can monetary stability be achieved. The historical experience thus provides a valuable point of reference not only for the study of ancient monetary reforms, but also for contemporary discussions on the regulation of digital currencies, the internationalization of the Renminbi, and the ongoing process of monetary digitalization.

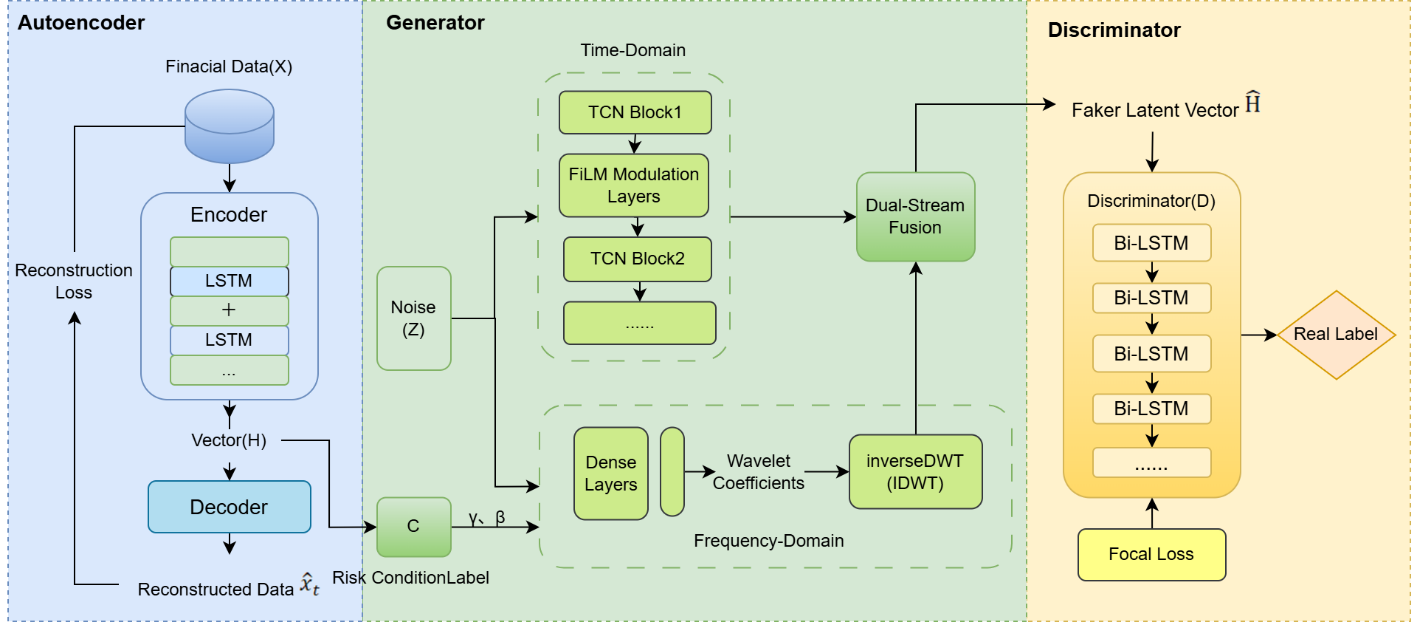

Owing to the low occurrence frequencies of extreme financial risk events, risk prediction models are prone to being dominated by the majority of the normal samples encountered during the pretraining process when using financial risk data. This weakens the ability to effectively learn abnormal characteristics and thus reduces the sensitivity and stability of the developed predictive model. To overcome these limitations, a data class-balancing model, Financial Wasserstein Generative Adversarial Network with Gradient Penalty (FinWGAN-GP), is constructed on the basis of the Wasserstein Generative Adversarial Network with Gradient Penalty (WGAN-GP) framework. Experimental results reveal that the FinWGAN-GP model achieves high-fidelity generation and expansion for high-risk samples, and a balanced dataset is conducive to improving the training effect of the early warning model. Through the integration of multisource heterogeneous data and Artificial Intelligence (AI) methods, the proposed model can identify potential financial risks earlier and more accurately, helping enhance the forward-looking and scientific nature of financial regulation.

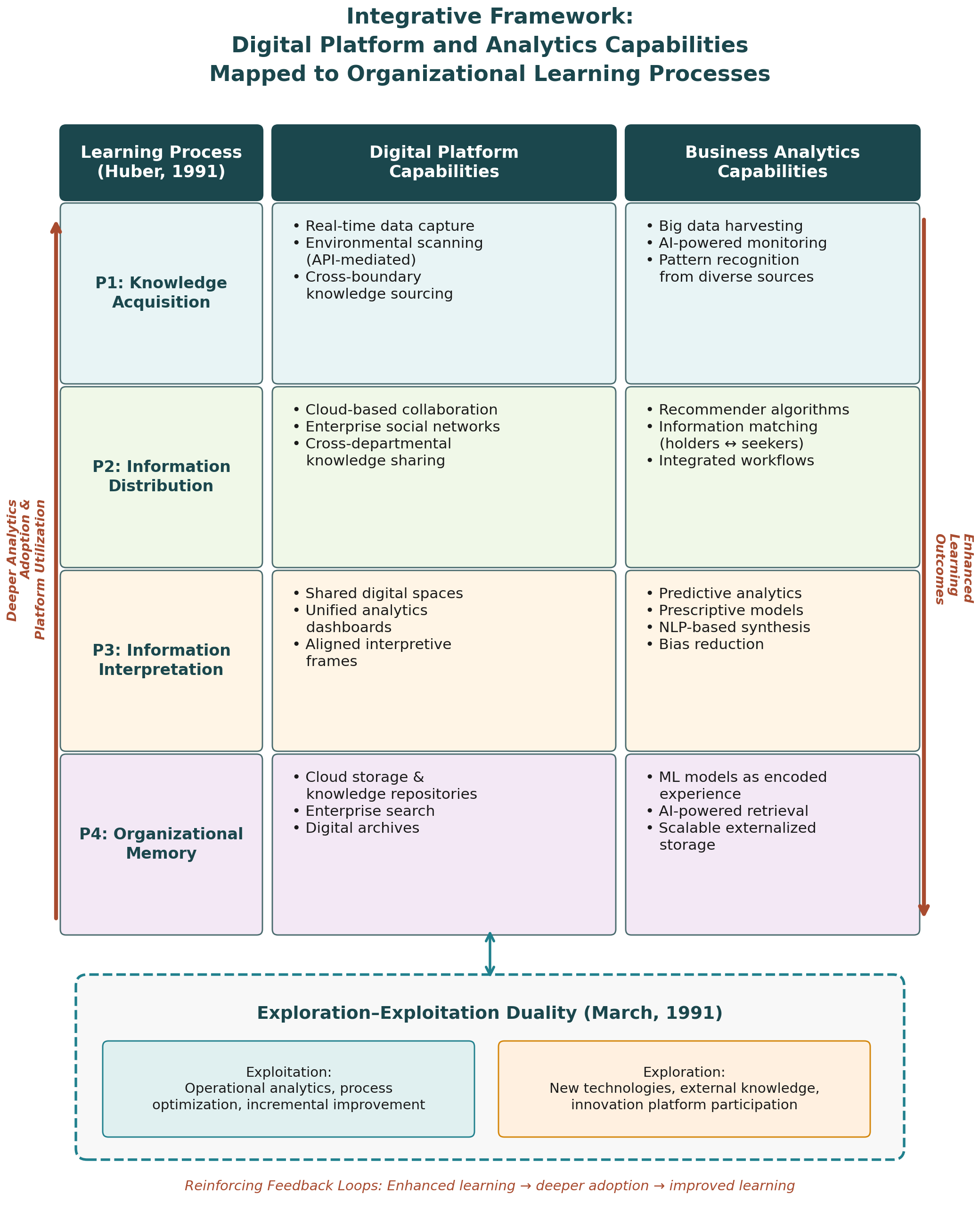

Digital platforms and business analytics are fundamentally reshaping how organizations acquire, distribute, interpret, and retain knowledge; however, few studies have systematically examined how digital platform capabilities map onto specific dimensions of organizational learning. This paper addresses this gap through a conceptual literature synthesis that integrates scholarship on digital platforms, business analytics, and organizational learning theory. Drawing on Huber's four-process model of organizational learning—knowledge acquisition, information distribution, information interpretation, and organizational memory—as well as March's exploration–exploitation framework, this study develops an integrative conceptual framework comprising four propositions linking digital platform and analytics capabilities to each learning dimension. The framework identifies reinforcing feedback loops through which enhanced learning drives deeper analytics adoption and digital platform utilization. Theoretical implications for updating organizational learning theory in the digital age are discussed, alongside practical implications for financial institutions pursuing digital transformation. Future research directions include empirical validation through firm-level surveys, industry-specific case studies, and longitudinal investigations of digital learning evolution.

Volumes View all volumes

2026

Volume 3July 2026

Find articlesVolume 3July 2026

Find articlesVolume 3March 2026

Find articles2025

Volume 2December 2025

Find articlesVolume 2June 2025

Find articlesVolume 2September 2025

Find articlesAnnouncements View all announcements

Journal of Fintech and Business Analysis

We pledge to our journal community:

We're committed: we put diversity and inclusion at the heart of our activities...

Journal of Fintech and Business Analysis

The statements, opinions and data contained in the journal Journal of Fintech and Business Analysis (JFBA) are solely those of the individual authors and contributors...

Indexing

The published articles will be submitted to following databases below: